Introduction

Recently, Lake Street Advisors, in conjunction with Bernstein Shur, hosted The State of Real Estate panel discussion at The One Hundred Club in Portsmouth, NH.

With a diverse audience of investors, developers, attorneys, and consumers alike, Lake Street Partner, Shawn Valliere, kicked off the discussion by highlighting the timeliness of the topic. Let’s take a moment to dive in here.

2023 was a volatile year for the real estate sector. Publicly traded REITs were moderately positive on the year, while private real estate generally experienced markdowns – the opposite of the 2022 story.

Factors causing the private markdowns include elevated interest rates that weighed on valuations, global investment volumes decreasing, and tightening lending conditions that caused less capital to enter the sector.

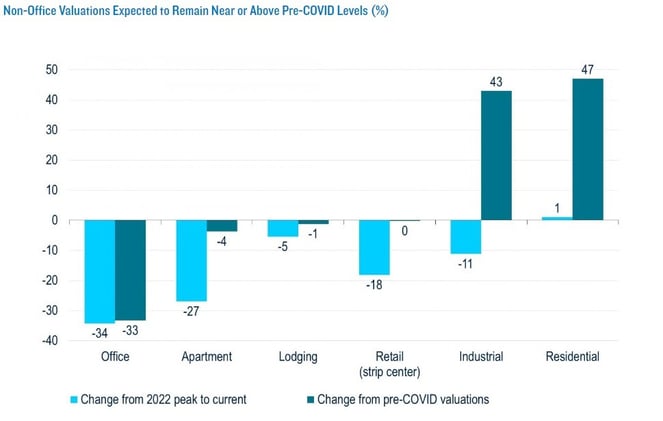

As the market is still repricing for higher interest rates, there is an increased focus on sector dispersion as office buildings have experienced increased vacancy and markdowns from pre-COVID valuations as shown below.

Source: PGM Fixed Income

Source: JP Morgan, Guide to the Markets

Source: JP Morgan, Guide to the Markets

Event Panel

Lake Street Wealth Advisor, Jim Machinchick, moderated our esteemed panel, which included the diversified perspectives of:

- Daniel Cummings: Partner and Chairman, Real Estate at Bain Capital

- Robert "Bob" Delhome: Founder and CEO of Charter Companies

- Rusty Mosca, CPA: Business Advisor, Nathan Weschler

- Jim Kerouac: Shareholder, Co-Chair of Real Estate Practice Group, Bernstein Shur

Top performing investors have the ability filter through the noise and maintain a consistent investment process throughout the peaks and troughs of market volatility. So, it should be no surprise that Dan Cummings sat with a level head and pleasant temperament as he delivered thoughtful responses about the state of real estate today.

Early into Dan’s (often not-so-positive) answers, he paused and joked, “Aren’t you glad you invited me?”

Yes, Dan we certainly are.

Let's get into the questions.

(Disclaimer: answers are paraphrased from panel discussions)

Question: As the Federal Reserve and broader market participants have continued to adjust expectations towards having higher interest rates for longer, what will be the impact on real estate valuations?

(Dan Cummings): It’s important to step back and understand what higher rates mean. In 2021, mortgage rates were 2-3% for ~65% LTV. Today those same loans are ~7-8% with LTVs at *maybe* 50%. Life science developments are looking at rates between 11-13%. All in, interest servicing costs are 2-3x greater than they were just a few months ago.

Cheap base rates during COVID-19 spurred a lot of buying activity. Many buyers bought without interest rate caps and undertook more leverage. Transaction volume began rising to where we were in early 2000s, and cap rates declined.

Recent transactions are looking like very early signs of distress. The most obvious example is office buildings, where work-from-home shifted the view of its value. Office space is down anywhere from 10-80% from peak and short-sales are occurring.

So how will changing rates affect real estate valuations? Too soon to tell, it’s a mess right now.

Question: How aggressive are the assumptions being used by investment managers in underwriting office buildings today?

(Dan Cummings): This depends on the eye of the beholder! I have seen a recent deal in DC done at $1000/foot and also seeing $600-$800 values dropping close to $150/foot. Work-from-home is presenting a challenge and affecting rates, especially in big tech cities and areas with long commutes. Quality is the differentiator –premium buildings are still getting their rent.

We should expect a big wave of foreclosures in the next 6 months, but we will also see some great wins during this volatility.

Office space is the most difficult part of the real estate asset class right now. Those that are investing now are making a bet that the top 10-20% of buildings will recover in value soon. Bet is the key word here (so use caution), these forecasts are not based on data.

Question: In this environment, everyone is looking for opportunity. Are there segments of real estate markets that have not historically had substantial institutional ownership, which are starting to gain traction with institutional investors? (Examples: Single family rentals a few years ago, self storage, etc.)

(Jim Kerouac): RV parks – high rent, low expense opportunities.

(Dan Cummings): Echo the RV parks. Additionally, self-storage, lab space and studios. There is a chronic undersupply of multi-family, affordable housing, and student housing.

(Bob Delhome): More capital flowing to complex land sights where there is an underlying environmental liability. These assets can trade at distressed values due to their requirement for strong infrastructure and complex permitting.

Question: Rusty, what are some tax trends within real estate, whether opportunity zones continue to be a focus or remain attractive. Are there any other current or upcoming tax impacts or changes that you have seen?

(Rusty Mosca): It’s worthwhile to do a cost segregation study which can lead to a bigger deduction and less on taxes. 1031 exchanges are common and fairly painless. 1031 exchanges take the gains from one property and roll it into another. The benefit of a 1031 exchange is a tax deferral (not mitigation), so there are embedded risks with this approach. The drawback of a 1031 exchange is that capital gains rates today are 20%. In 2025 these laws sunset and are unlikely to be favorable. Acknowledging the national deficit and cost of capital, capital gains rates are unlikely to decrease; therefore, it can be advisable to pay the tax as promptly investors are able to.

What is a cost segregation study? A cost segregation study is a process that looks at each element of an investment property, splits them into different categories, allows the investor to benefit from an accelerated depreciation timeline for some of these building components[1]. It is a tool that allows investors to more quickly deduct the appreciation of their property.

What is a 1031 exchange? 1031 exchange allows an investor to defer capital gains taxes on an investment property by selling the property and putting the proceeds into a like-kind property, which is a property that is similar in nature and value[2].

Question: Without sounding like I am asking “What’s the hot stock to buy!?” - What types of real estate transactions may be most attractive to high-net-worth individuals in the current economic and tax environment?

(Dan Cummings): The opportunity forthcoming in real estate is exciting, investors just need to try to be patient.

There are a lot of sponsors looking to raise capital for mezzanine debt (high yields over a short period, small multiple on invested capital).

Opportunity will come in the form of being able to buy from certain sellers below replacement costs. These opportunities have can ~12-15% unlevered returns. I have seen a few things come their way recently, opportunity stems from liquidity needs of the seller.

Reiterating that patience is key – these things take time. Investors shouldn’t be worried about whether they should be doing something now. It’s best to partner with advisors who can spot value.

(Bob Delhome): There are a lot of bright spots in the market, particularly in distressed land. In Massachusetts, there is pressure to create additional affordable housing. This affordable housing is going to have to be created on distressed land, which highlights the opportunity in undeveloped, complex land sites.

Question: Maybe not everyone is optimistic about real estate, Dan - what are the best methods of shorting commercial real estate today?

(Dan Cummings): There are plenty of different ideas for hedging real estate. However, they always seem to come up short since it is challenging to find something so tightly correlated that it makes sense. Currency hedging is a consistently utilized strategy.

Question: If anyone over the past couple years has done a renovation or update to their property, I am sure you have felt the impacts of inflation. With this high inflation and strains in supply are you seeing any signs of relief in executing on projects?

(Dan Cummings): Costs have gone up 20-30% in the past few years and the rise in interest rates has made the justification for new builds very difficult. The life sciences sector had 11million of square feet due to be delivered in the next 4-5 years. We should expect that maybe 30% of that will ultimately be built. Bain is financing with cash where they can.

(Bob Delhome): Commercial (non-residential) development has gone off a cliff and the cost of construction is not going down. On the positive side, infrastructure funding has created a lot of horizontal construction opportunities.

(Rusty Mosca): Contractors (especially small ones) are very busy right now. There is not a lot of opportunity in the workforce to reduce costs.

Question: You have all been in the business for decades and have seen many real estate market cycles, what are your thoughts on where we go from here?

(Dan Cummings): Sam Zell had a mantra in the 90s – “stay alive until ’95.” This mantra still exists and now its “stay alive until ’25.”

This recent real estate cycle has been one of the sharper drops that we’ve experienced. In contrast, the GFC showed evidence of cracks 1.5 years beforehand and it took 3-4 years to recover. In general, today’s ¬¬operating conditions (other than office buildings) look very strong. We are not oversupplied – if anything we’re undersupplied.

Technology in the 1990s that was used to figure out where we were in the market is much different than what we have today. This will enable a faster recovery, but we could certainly see a year or two of tough conditions.

(Bob Delhome): This environment presents opportunity and there is a chance to see some growth. A great example is that value-add real estate performs better in down years than up years.

(Jim Kerouac): Right now, people that are flexible and creative have the best chance of outperformance.

(Rusty Mosca): My view from the tax perspective is that there is an opportunity to move ownership of properties at lower valuation for lower basis and a discount. This is especially a great time for asset transfers for families that want to keep the real estate over the long term.

Conclusion

As our panelists highlight, with volatility comes opportunity. Today’s real estate environment has provided periods of uncertainty and unprecedented changes in the market. During these times, it is more important than ever for investors to stay patient, remain focused on fundamental valuations and maintain a consistent, long-term investment strategy.

Stay alive until ’25 might be the mantra but we’ll be paying close attention to opportunities along the way. At Lake Street, we believe that real estate serves a valuable role in the portfolio, offering growth potential, inflation protection, and diversification from public equities. We favor private investments in areas of the market that have opportunity for outperformance and partner with managers that have a demonstrable and sustainable edge. If you would like to hear more about Lake Street’s investment philosophy and current opportunities in the market, please do not hesitate to reach out to us.

[1] Billings, Lisa (2021). What is a Cost Segregation Study? Warren Averett.

[2] Brock, Melissa (2023). 1031 Exchange: What Real Estate Investors Need to Know. Rocket Mortgage

If you enjoyed this article, please subscribe to get our insights delivered straight to your inbox.