There’s no shortage of investment professionals who’ve weighed in on the active vs. passive investment management debate over the years. Most of these points of view approach the question as a black and white, right or wrong proposition. Proponents of active management like to talk about downside protection in bear markets and their abundant experience as long-term investors. Indexing enthusiasts point to the considerably lower cost of passive investing and its notable success relative to active managers in aggregate. My answer to the question of whether it’s better to hire an active manager or go the passive route of indexing is “it depends.”

Successful active investing depends on three distinct conditions. First, there must be an opportunity/inefficiency for an active investor to exploit. Second, an active investor must have the skills necessary to take advantage of and profit from that opportunity. Third, you or your advisor must have the ability to identify the best, most highly skilled active managers. In this article we will discuss the first condition: opportunity/inefficiency.

The objective of active management is to exploit mispriced securities in a given market and produce returns in excess of the market average. In order to do this well enough to justify the fees charged and taxes generated by the active manager, the target market must have ample mispricing to leverage. Theoretically, as the graphic below shows, a larger frequency and magnitude of mispriced securities equates to an attractive opportunity set (what we refer to internally as an excellent “fishing hole”) for a given strategy whereas a low frequency and small magnitude of mispriced securities translates to an unattractive opportunity.

The point here is that all the investment skill in the world is effectively useless if there aren’t any attractive opportunities to make use of it.

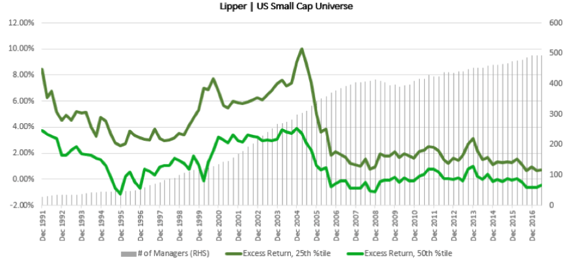

Turning to a real life example, let’s examine the US Small Cap universe, which is often cited as an opportunity rich market for an active manager. The “go to” narrative here is that these stocks are more inefficient because there is less sell side research coverage relative to larger cap stocks, which is true, but does that really matter when there are close to 500 US Small Cap mutual funds1? That equates to a ~4-to-1 stock to investment team ratio across the investable universe of ~2,000 stocks. This ratio also ignores the sell side research coverage as well as hedge funds actively investing in the US Small Cap space. How can that possibly lead to pricing inefficiencies large enough to justify fees and expenses? The answer, as I see it, is that it doesn’t. There is simply too much competition for exploiting the difference between calculated intrinsic value and market prices to justify the fees paid and taxes generated by an active equity strategy in US Small Cap, as typically executed.

The chart above helps illustrate my point. The data is based on 5-year rolling returns calculated quarterly. Over the last ~25 years, the number of managers has steadily grown and the excess return from the median and 25th percentile manager in the US Small Cap space have diminished. Where you once were rewarded with ~4.4% in annualized excess return, on average, from selecting an active manager in the 25th percentile in the 1990s, you now average a small fraction of that at around 1.6% annualized (ten years ending 6/30/2017), pretax. This also assumes that you have selected a manager in the top quartile, a topic we will discuss in a future article. In short, investors and allocators are better off focusing their time and energy on more promising opportunities and employing a passive option in US Small Cap, especially for a taxable investor.

Conclusion

For investors of substantial wealth, it’s not enough to treat the active vs. passive decision as a black and white proposition. Advisors who embrace the shades of gray and understand what it takes to be successful in manager selection can provide their clients with better opportunities to meet their long-term objectives. By starting with first principles and taking a logical approach to capital allocation within client portfolios, we build diversified portfolios combining passive strategies with active managers where the three conditions outlined above have been met. For more on this topic, feel free to reach out. We enjoy the questions and discussion.

1 Per the Lipper Database on US Small Cap mutual funds, there are 494 funds filtered for primary share classes only.